Why the Numbers 75, 15, and 10 Matter for Your Money

Sep 28, 2025Hello Stoic Investors,

How many of you enjoy planning for the future?

Well, I can’t see how many hands are raised out there, but I can assure you I’m one of those people!

I like the idea of having things under control and being able to enjoy life without living in chaos or feeling at the mercy of events.

This mindset especially applies to how I manage my money.

Having a clear plan for my income helps me stay relaxed and prepared for whatever life throws my way.

And to show you how I organize my money, I’ll respond to this question:

I want to focus on just one rule that I use and find especially practical and effective:

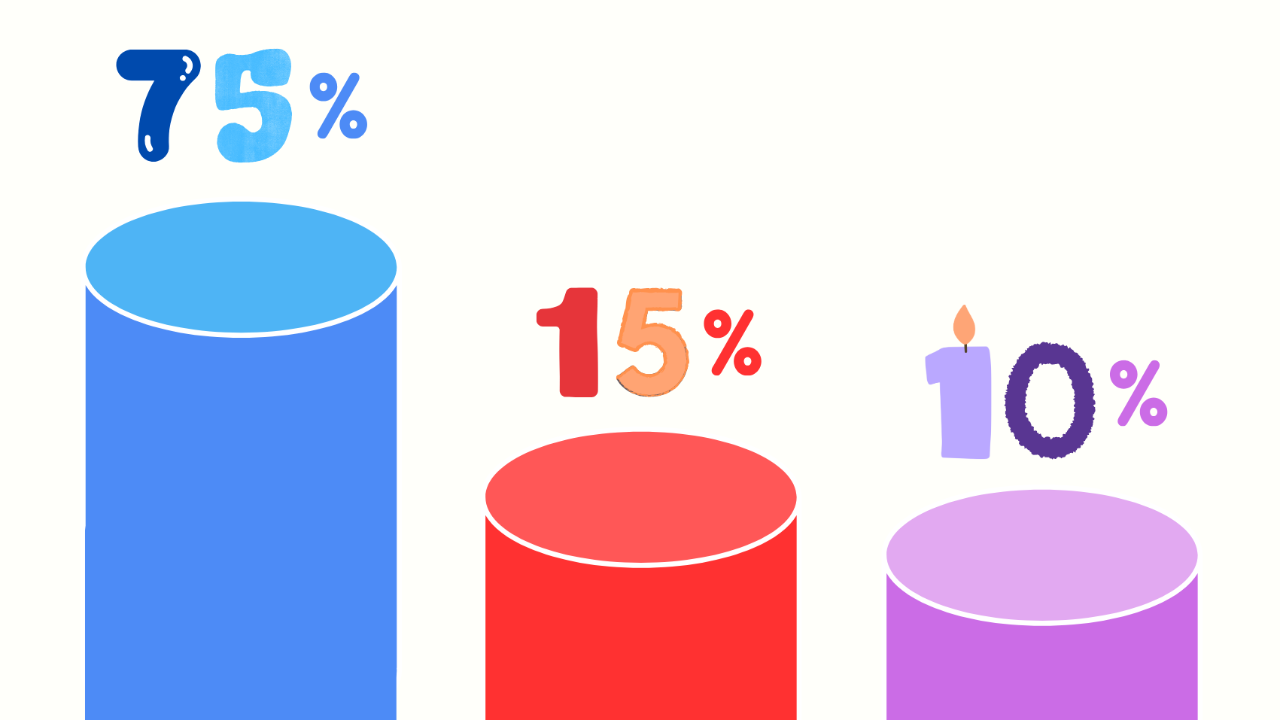

The 75-15-10 rule.

What do you need to put this rule into practice?

Before anything else, you need a budgeting system — a simple way to track how much money comes in, how much goes out, and where it all goes.

If you already have a planner you like, that’s great — use that.

But if you don’t, I’ve created one that you can download for free HERE.

This small step makes it much easier to take control of your money and follow the rest of the plan with confidence.

Now that you’ve set up your budget planner, it’s time to divide your monthly income into these 3 categories:

75% for Essentials

The first and most important category is your essential expenses — the things you need to live and function day to day.

The rule is simple: aim to spend no more than 75% of your monthly take-home income on these essentials.

What counts as an essential expense?

- Rent or mortgage

- Utility bills (electricity, gas, water, internet)

- Groceries and basic household items

- Transport (fuel, public transport, car insurance)

- Phone bill

- Childcare or school-related expenses

- Any recurring payments you absolutely need to make

Why is this step important?

Because for many people, essential costs slowly expand without them noticing.

Subscriptions, upgrades, lifestyle changes — they all add up.

Keeping your essentials within 75% ensures you’re not overspending on your present lifestyle at the expense of your future goals.

If your essential expenses currently take up more than 75%, don’t worry.

The goal isn’t to be perfect overnight — it’s to start adjusting, step by step.

What matters is that you’re becoming more intentional with your money!

15% for Investing

Once you’ve covered your essentials, the next step is to focus on your future — and that means investing.

The rule here is: aim to invest 15% of your monthly take-home income.

This isn’t about gambling in the stock market or picking the next big thing.

It’s about building long-term financial security with a steady, low-risk approach.

But where should you invest?

It depends mainly on your age and goals — here’s a simple guideline to help you get started:

- If you’re over 40: consider investing through a SIPP (Self-Invested Personal Pension).

A SIPP is a retirement account with strong tax advantages.

Money you invest here grows tax-free and can be accessed when you retire.

Plus, the government tops up your contributions with a tax relief bonus — essentially free money added to your investments.

- If you’re under 40: a great place to start is a Stocks & Shares ISA.

This is a flexible, tax-efficient account where your investments can grow over time — and you can withdraw the money whenever you want, without paying tax on the gains.

It’s perfect if you want to invest but still have access to the money in the future.

A simple way to start is by investing in index funds or ETFs (exchange-traded funds).

These are low-cost investments that spread your money across hundreds (or even thousands) of companies, reducing risk while still allowing your money to grow.

For example, a global ETF might invest in the top companies across the US, UK, Europe, and Asia — giving you instant diversification with just one investment.

This step is important because money kept in a regular savings account loses value over time due to inflation.

Investing allows your money to grow faster than inflation, which means you can actually build wealth instead of just holding on to it.

10% for Emergency Fund

The final 10% of your income should go toward building an Emergency Fund — a financial safety net that protects you when life doesn’t go as planned.

The rule here is: aim to build up enough savings to cover 3 to 6 months of essential living expenses.

Think of it as a personal insurance policy: it’s not exciting, and you hope you never need it — but when something unexpected happens, it can make all the difference.

It’s for real, urgent, and unexpected expenses — things like:

- A surprise car or home repair

- Medical bills

- Losing your job or needing time off work

- Emergency travel

- Unexpected costs that aren’t part of your normal budget

This is not a fund for sales, holidays, or treating yourself.

It’s money you don’t touch, unless you truly need it.

You don’t need to reach this amount overnight.

Just set aside 10% of your income each month until you get there.

And here’s the good news: once your emergency fund is fully funded, you can stop adding to it if you want.

At that point, you can take this 10% and add it to your investments.

That means you’ll go from investing 15% to investing 25% of your income — a huge step toward long-term financial freedom.

A Practical Example

To help you better understand how this works in real life, let’s look at an example where you earn a £4,000 salary.

Here’s exactly how the 75-15-10 rule would apply in this situation:

This 75-15-10 rule is just one of many budgeting methods out there.

I like it because it’s reasonable and takes into account different life scenarios and unexpected events, helping you prepare for the future without feeling overwhelmed.

But beyond any specific rule, what really matters is having a clear plan — one that puts you in control of your money, instead of letting your money control you.

No matter which budgeting strategy you choose, the key is to take charge, be intentional, and make your money work for you!

So, note down this 75-15-10 rule and start budgeting today:

1. 75%: Spend on essentials like rent, utilities, and groceries;

2. 15%: Invest regularly using tax-efficient accounts like SIPP or Stocks & Shares ISA;

3. 10%: Save for your emergency fund, then add this amount to your investments once it's complete.