Do you know what my favourite type of investment is?

Jul 06, 2025Hello Stoic Investors,

Today I have a question for you:

If you had to guess what’s my absolute favourite thing to invest in as a long-term investor...

What would you say?

And for my long-time readers you should know this by now, given that I talk about it more than I talk about Marcus Aurelius or how good Italian coffee is (plus, the answer’s kind of hiding in the subtitle anyway).

Any guesses?

Well, I’m talking about ETFs!

An ETF (Exchange-Traded Fund) is basically a basket of stocks or any other assets, like bonds, commodities, or real estate, with similar characteristics.

Imagine you don’t want to buy 100 different companies one by one.

An ETF does it for you — it combines many companies into one single investment.

For example:

- A World ETF invests in companies from all over the world.

- A Tech ETF might include only companies like Apple, Microsoft, and Google.

- A S&P 500 ETF includes the 500 biggest companies in the US.

And that's why ETFs are diversified, which means your money is spread across many companies.

That makes it safer, because if one company drops, others can balance it out.

But here’s the part no one tells you:

99% of people are picking the wrong ETFs.

And they end up paying too much, taking too much risk, or growing their money slower than they could.

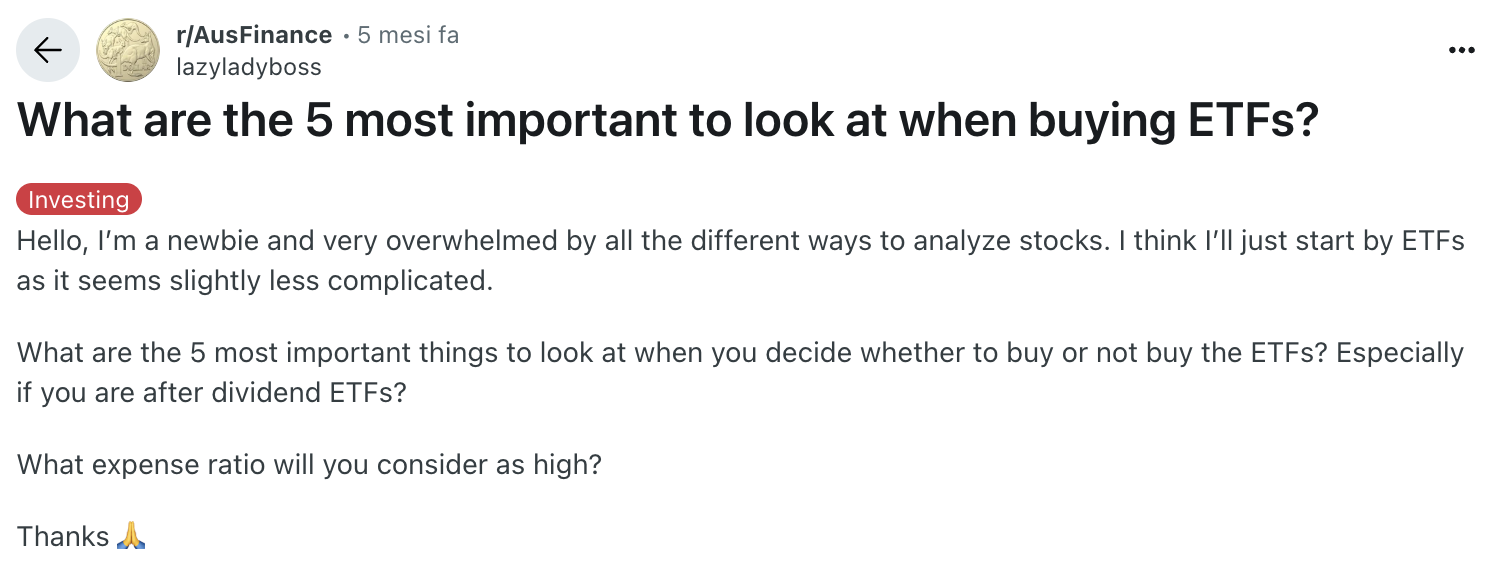

That’s exactly what someone asked in a Reddit post:

Let’s try to answer his questions — and make sure you’re in the 1% of investors who actually pick the right ETFs.

These are the 5 things to check before buying:

1. Benchmark

Every ETF follows a “benchmark” — basically, a set of rules that says what the ETF will invest in.

For example, the S&P 500 index includes the 500 biggest US companies.

So if you buy an ETF that tracks the S&P 500, you’re investing in those companies.

If you don’t understand the benchmark, don’t buy the ETF.

Stick with simple ones like the MSCI World (global developed markets), FTSE All-World, or the S&P 500.

2. Return

You’ll often see charts showing how much an ETF went up or down over time.

But don’t just look at the number — ask why it performed that way.

Is it because it’s invested in fast-growing companies? Or maybe it’s focused on a region that did well recently?

And compare it with other benchmarks.

If it’s performing worse than a similar ETF, that could be a red flag.

3. Cost

Every ETF charges a small annual fee, known as the Ongoing Charge or Total Expense Ratio (TER).

This is taken automatically every year from your investment.

Aim for ETFs that charge around 0.1% to 0.2%. Anything above 0.5% is usually too expensive for what you get.

It may not sound like much, but over time, high fees can seriously eat into your returns.

A cheaper ETF means more of your money stays invested and compounds.

4. Replication Method

This tells you how the ETF tries to copy its benchmark.

There are 3 main types:

- Physical replication: the ETF actually buys all the stocks in the index. This is the most transparent and reliable method.

- Physical sampling: instead of buying all the stocks, the ETF buys a representative sample. This is common for large indexes with hundreds or thousands of stocks — and it still works well while keeping costs low.

- Synthetic replication: the ETF doesn’t buy the actual stocks but uses financial contracts (called derivatives) to mimic the performance of the index.

For beginner investors, it’s best to stick to physical or physical sampled ETFs.

Avoid synthetic ETFs — they’re more complex and introduce extra risks you don’t need.

5. Dividends

Some ETFs pay you cash every few months — this is called a distributing ETF.

Others automatically reinvest that money back into the ETF — these are called accumulating ETFs.

Personally, I prefer accumulating ETFs, especially if your goal is to grow your money long-term.

Why?

Because with distributing ETFs, the dividends you receive in cash might be taxed every year — even if you don’t plan to use that money yet.

With accumulating ETFs, the dividends are reinvested automatically, and you avoid paying dividend tax yearly.

That means your money grows faster, and you don’t have to worry about reinvesting manually.

But there’s also a second reason: in many cases, companies that don’t pay dividends are actually reinvesting that money to grow faster — launching new products, expanding to new markets, or hiring great people.

That can lead to bigger long-term returns for you as an investor.

So with accumulating ETFs, you’re not just being tax-efficient — you’re also often backing businesses that are focused on growth.

Now you know what to look for.

Take 5 minutes before your next investment and check:

Do I understand the benchmark? Why is the return what it is? What are the costs? How is it replicated? And how does it handle dividends?

That small effort will save you time, money, and regret down the line!

So, note down these 5 key-points and start investing today:

1. Benchmark: Make sure you understand what index the ETF is tracking;

2. Return: Check how the ETF has performed and why it’s higher or lower than the market. Look at what it invests in;

3. Cost: Avoid ETFs with fees over 0.50%, the best ones charge around 0.1%–0.2%;

4. Replication: Choose physical or physical sampled ETFs and avoid synthetic ones — they’re more complex and riskier;

5. Dividends: Go for accumulating ETFs if you want long-term growth and fewer taxes.