INVESTING COACH EXPLAINS: How To Help Your Parents Plan For Their Retirement

Mar 24, 2024Hello Stoic Investors,

Today I'm going to answer a personal finance question from Reddit.

This is the post in question:

The first thing we need to do is to make some assumptions about their situation.

First, let's say they will both live 20 more years.

Second, they spent more money last year than they usually do. So, we'll guess they can spend 20% less

this year, making it about $130.000.

Third, they want to leave $300.000 from their $800.000 as inheritance for their children.

Based on these assumptions, let’s try to solve the two main problems they're facing:

Keep their $130.000 lifestyle for the next 20 years and leave something for their children.

The first thing we can say is that they need at least an extra $60.000 per year to maintain their $130.000

lifestyle, because they already get $70.000 from their pension.

But how can they find this extra $60.000?

Let’s consider some scenarios.

The worst scenario: They don’t invest the $800.000

If they keep the $800,000 in cash without investing it, they can live their current lifestyle for about 13 more

years.

This is because they need $60.000 a year, and if you divide $800.000 by $60.000, you get roughly 13 years.

And so, by not investing, they won't reach the hoped-for 20 years of funds. So, it's clear we need to find a

better solution.

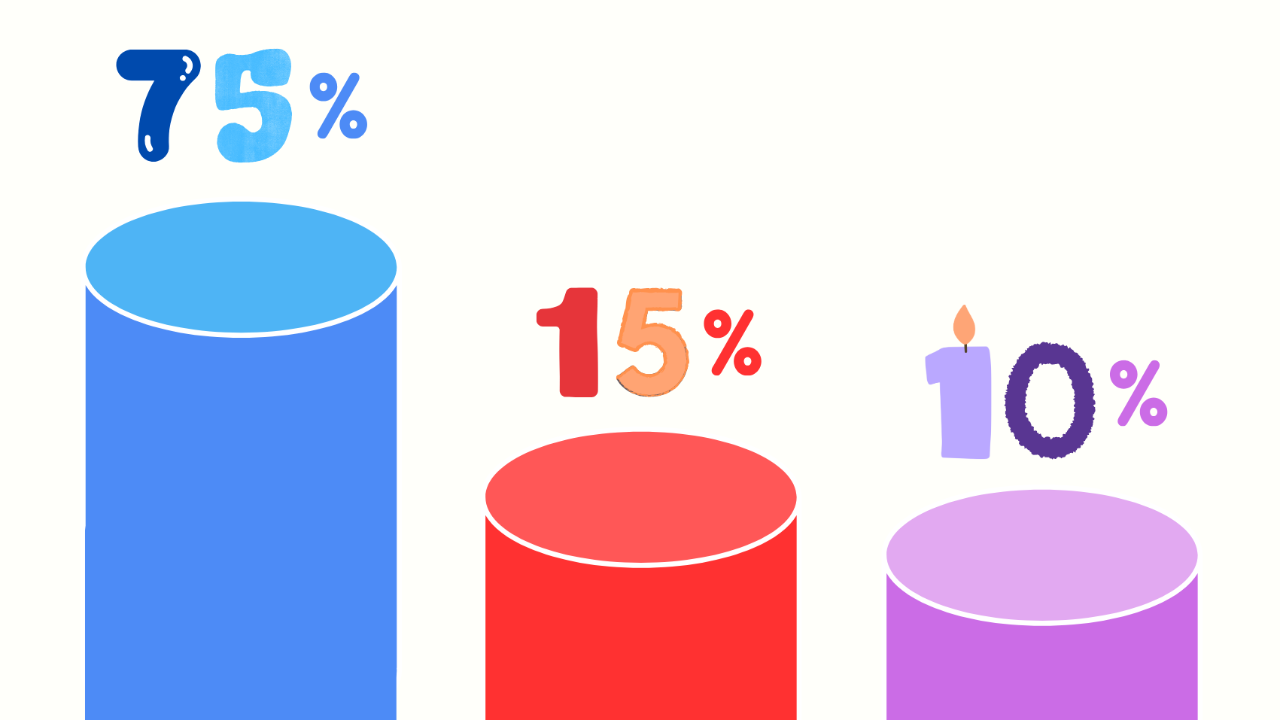

A better (but not the best) scenario: They invest the $800.000 in stocks

If they invest all $800.000 in stocks, aiming for a 10% annual return, they'd earn $80.000 a year, which is

even better than the $60.000 they need.

However, putting everything in stocks is risky because the market could crash.

A crash could mean losing 40% in a year, and it might take five years to recover.

That's why this isn't the safest plan.

The best scenario: They invest the $800.000 in long-term bonds

If they choose to invest the $800.000 in long-term bonds, they’d have a 5% yearly return, which is $40.000

per year.

To cover the remaining $20.000, they can sell a part of the bonds each year.

In fact, by selling $20.000 worth of bonds from the $500.000 they plan to use, they can sustain this for about

25 years without touching the $300.000 set aside for inheritance.

Of course, the more bonds you sell the smaller will be the return of the bonds, but it'll take years for this

impact to be significant.

This approach is safer than stocks because it avoids market volatility.

They can also be a little more aggressive, investing the $300.000 in the stock market for their children and

$500.000 in long-term bonds. It’s slightly different, but overall, the strategy is the same.

This depends on how comfortable they are and if they actually want to save something for their children,

which I'm fairly certain every parent wants to do.

So, if you are in a similar situation, note down these three key points and start investing today:

1. Don’t invest all your money in stocks: Putting everything in stocks is risky because the market

could crash, causing a 40% loss in a year.

2. Invest in long-term bonds: This approach is safer than stocks because it avoids market volatility.

3. If you want to be a little more aggressive, invest a part of your money in the stock market and the

rest in long-term bonds.